Congestion Management Technology that Mitigates no Congestion

Congestion Management Technology that Mitigates no Congestion

This edition looks at the big business of managing congestion in Australian ports, the largest electric truck order in Australia and Toyota's hydrogen bet.

Earlier this year, I wrote about the traffic mitigation fee (TMF) imposed on transporters who deliver containers to the Los Angeles port in the U.S. which had (almost) no effect on mitigating traffic congestion. Shifting across the Pacific to Australia to find its port congestion management model, its limited success in mitigating congestion and fantastic success in producing a 💩ton of cash for terminal operators. The recent Australian Competition & Consumer Commission (ACCC) ‘Container stevedoring monitoring report’ which monitors Australian terminal operators’ behaviors (stevedores is synonym of terminal operator) details how landside transport fees now account for more than 40% of terminal operator income, most of which generated using the vehicle booking systems (VBS), originally designed to tackle truck congestion at Australia’s ports. One might say that the transporters are in a VBS – a Very Bad Situation.

As a sidenote, I spent the better part of the past decade working and researching in container shipping logistics , half of which I spent conducting my applied doctoral research in managing congestion in ports using technology. Some of the ideas in the latter part of this post have been developed during my PhD research and are the result extensive (and sometimes exhausting) discussions with co-authors and friends whom I thank for their contributions.

I hope you’ve enjoyed interconnected so far, a Happy New Year to you all and I’ll see you in 2023!

Port Congestion and Vehicle Booking Systems

Container transport is rather odd. Sending cargoes from say Asia to Australia means contracting a shipping company for ocean carriage. Once the ocean carriage is agreed, the land transport is organised. The shipping company has its own agreements with port terminal operators. In this sense, the choice of terminals is determined by the choice of shipping line. A peculiarity of this arrangement is that the land transport operator often has no actual say in which terminal to pick-up from or deliver containers to. That is entirely determined by the shipping line choice. Hence, prior to the introduction of VBS, most transport operators (especially trucking) did not even have contracts or service level agreements with terminal operators.

In the absence of service level agreements between transporters and terminal operators, congestion at port terminals proior to the introduction of vehicle booking systems (VBS) was often nobody’s problem. Truck waiting times at Australian ports exploded. Before 2011, trucks took 50 minutes, on average, to load or unload containers at Australian ports. VBS were brought in to manage truck arrivals at terminals in the hope that the technology would ease congestion by improving coordination and directing truck arrivals at terminals outside peak hours (9am to 6pm). New South Wales (NSW) went as far as introducing the Port Botany Landside Improvement Strategy (PBLIS), a government-led initiative to manage performance between terminal operators and transport operators – in essence a pricing tribunal, levying fines on one side (transporters) or the other (terminal operators).

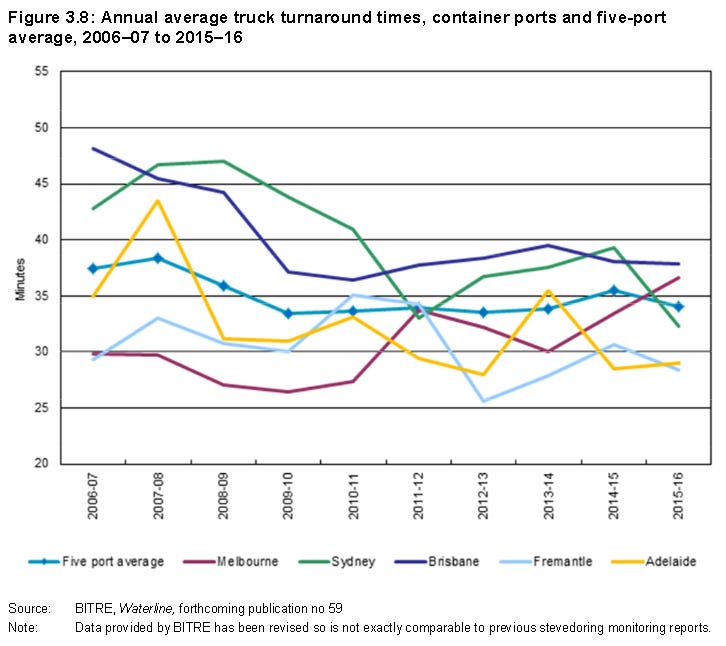

The initial impacts of the VBS and the PBLIS scheme were remarkable. The graph above shows the steep decline in truck turnaround times (how long a truck spends on the terminal to load and unload containers). Truck turnaround and waiting times almost halved in NSW port terminals. Although fluctuating, truck waiting times rarely returned to previously experienced levels. However both solutions came with several unintended consequences. Irrespective of location or VBS system however, the technology failed to a great extent to achieve the stated goal of shifting truck arrivals to outside peak hours arrivals and has certainly failed to deliver any modal shift benefits (p.21). So, how did waiting times decrease? Congestion shifting and cost shifting.

Congestion was shifted outside the areas where it was measured. Truck turnaround and waiting times are counted while trucks are on the terminal premise. In NSW, a truck marshalling area was built for trucks arriving before their appointment. The waiting that took place within terminal boundaries now takes place outside. Transporters adapted. Many purchased A-double truck combinations that can carry two 40ft containers (4 TEU). These are generatlly used totransport containers to their own warehouses (often located near ports) where the containers are then shifted to semi-trailer trucks for deliveries to customers. All these big trucks and forklifts needed to shift containers from one truck to another are expensive. Hence, costs mostly shifted to transporters to adapt to the congestion management.

Not The End of Port Congestion Problems

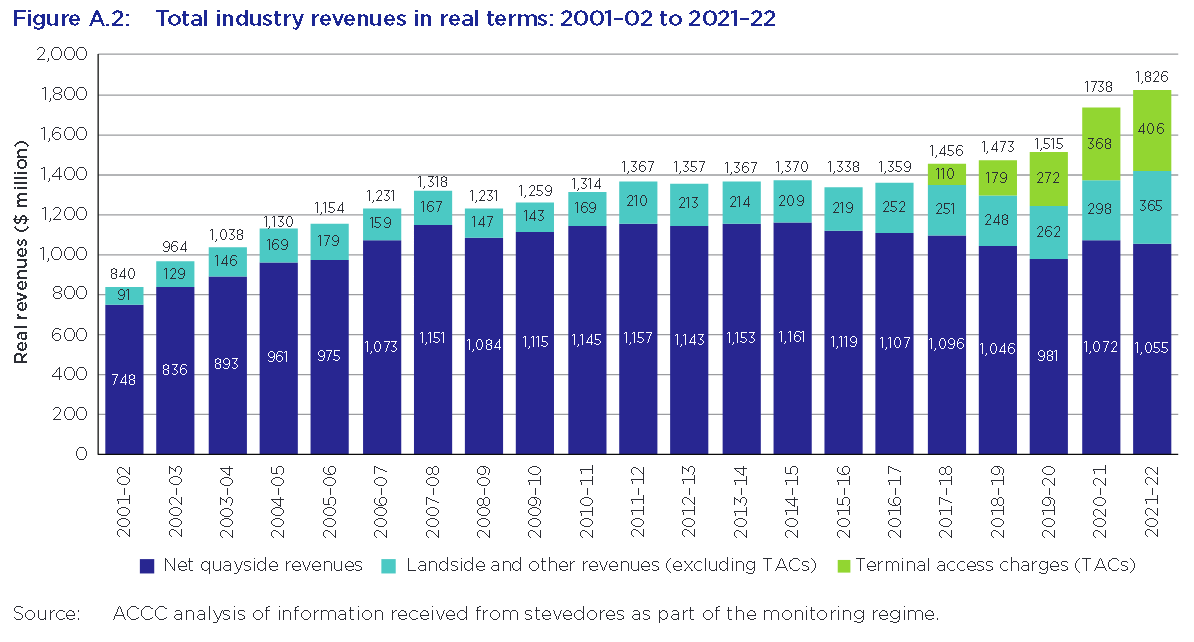

If you imagined that was the end of transporters pains with congestion management and technology, you’re in for a shock. Terminal operator land-side charges and revenues that had been slowly increasing since the introduction of the VBS took off since 2018. In 2011, land-side revenues accounted for 18% of terminal operators’ revenue. In 2022, they accounted for 42% (see graph below). Why? New technologies and terminal automation were supposed to increase terminal efficiency and decrease costs! Has terminal operators’ land-side efficiency decreased 2.5 times since 10 years ago? If pricing reflected costs, one might be inclined to believe this theory.

The most likely explanation seems to be that the exorbitant increase in prices is due to the terminal operators’ market power exacerbated by the VBS. Terminal operators operate in an oligopoly in Australia: within each state, a few operators provide stevedoring services, mainly to local customers. Local customers are usually called the “captive hinterland” because they don’t have too many viable port options - A business in the ourskirts of Sydney will rarely deliver its containers to Adelaide. Remember that transport operators do not have much of a choice in terms of which terminal operator they pick-up containers from? This restricts transporters’ ability to respond to land-side price increases. Traditional market theory suggests that a price is the intersection between supply and demand. When demand is inelastic, such as in this case, the concentrated market power terminal operators have means that they can increase prices at their leisure. On the seaside, where terminal operators face an oligopoly of ocean shipping lines, the cost pressures reverse. Terminal revenues in real terms from seaside have been on a consistent decline for close to ten years.

The VBS plays a role in exacerbating terminal operators’ market power as it allows scalable monetisation of somewhat arbitrary behaviours. It is expensive to measure the exact time of arrival or departure manually. It is straightforward and scalable (i.e., cheap) using technology. At NSW ports, through the VBS, 15 transport operator behaviours are monitored and fined as opposed to 2 behaviours of terminal operators. That’s on top of other charges that must be paid to access the terminal.

Tackling Port Congestion Head-on

Vehicle booking systems (VBS), originally brought on in Australian ports to manage congestion have proven to be extremely effective at generating revenue streams for terminal operators by allowing them to leverage their market power on transporters while proving somewhat ineffective at managing congestion. The problem is therefore twofold: (1) how should congestion be managed differently and (2) how should the market power between terminal operators and transporters be balanced.

Congestion, although treated as a distinct problem, is usually a symptom of intersecting supply chains which requires a supply chain approach to tackle. Congestion can happen because of insufficient infrastructure but that’s rarely the case, otherwise congestion would never clear. Often, congestion is caused by the ways in which different actors in supply chains interact (for instance, drivers arriving at terminals at the same time because of overlapping start times) or the information they do or don’t share. VBS can be the supporting technological component of that approach which should be used after the approach is determined. For instance, part of the reason why truck arrivals at terminals remain concentrated during the day is because the customers’ warehouses only work during the day. It’s pointless for a transporter to pick-up a container in the middle of the night to let it sit on a trailer for six hours until the receiver’s warehourse opens for business. Agreeing on a mechanism to align working times along the supply chain first, then using the technology to monitor behaviours is much more likely to succeed than the current approach of fining transporters into oblivion.

Balancing of market powers between transporters and terminal operators can be internally or externally driven. Transporters can aggregate (either in alliances or through horizontal integration) to improve their market power. Ocean shipping companies have successfully used the alliance model to increase their bargaining power with terminal operators. Ultimately, this model led to horizontal integration. Externally driven balancing can be achieved through regulation and oversight. The NSW PBLIS scheme tried to instantiate this oversight but failed, possibly because of a key faulty assumption that pricing mechanisms are the way to mediate relationships between different parties in supply chains. However, regulation that limits the extent and types of additional terminal charges could help. Free market economic theory seems to fail when faced with oligopolies.

Technology is rarely the solution to social problems and interactions but tends to reinforce and exacerbate the disfunctional aspects of these interactions. The effects of vehicle booking systems on port congestion (and mainly terminal operator revenues) in Australia are an example of this mechanism at play. Ultimately, tackling congestion requires tackling the actual problem (queuing) and the market power imbalance. In either case, technology can contribute to the solution but cannot be the solution.

In Other News

Australia’s Largest Electric Truck Order

Team Global Express (formerly Toll Global Express) recently announced an order of 60 battery electric trucks for their distribution centres in Sydney. The trucks and their charging infrastructure costs are estimated at AU$ 44.3 million of which AU$ 20 million are funded by the Australian Federal Government.

Anecdotally, Volvo trucks operate a 5-year battery leasing model, during which time the battery range is expected to drop to around 80%. After the five years, the battery is replaced. It is unclear whether the 44 million dollars cover the battery lease or other costs. However, the total amount does indicate some general costings for trucks. The cost per truck and charging station (assuming one station per truck) stands at around AU$ 738,000. After the Government funding, the cost is at AU$ 400,000. If chargers cost around AU$ 100,000, that still leaves the trucks at AU$ 600,000 before the Government funding. That’s THREE times the cost of a fossil fuel powered truck. I’d like to see the emissions and costs modelling for these trucks to understand how this decision makes sense.

Toyota’s Hydrogen Bet

Toyota, the least environmentally friendly auto-maker according to Greenpeace, have just released plans to develop a hydrogen powered Hilux based on the Mirai platform. This development comes as Toyota’s President, Akio Toyoda, questioned the exclusive pursuit of electric vehicles for future mobility:

“That silent majority is wondering whether EVs are really OK to have as a single option. But they think it’s the trend so they can’t speak out loudly.

(Akio Toyoda, Source: WSJ)

This announcement comes at a time of renewed scepticism of hydrogen’s potential to contribute to the renewable energy transition. The interesting thing about this particular piece was how it was quick to discount hydrogen vehicles’ potential while failing to mention any of the same shortcomings in electric vehicles.

“While hydrogen is touted as a clean-burning fuel and it continues to build momentum in the heavy transport sector, most of it is not produced using renewable resources and is known to be difficult to handle and transport.

Although there is a large amount of industry discussion around the production of ‘green hydrogen’, 96% of the world’s hydrogen usage is classified as ‘grey hydrogen’. It’s estimated that for each kilogram of grey hydrogen obtained, 10kg of carbon dioxide is produced.”

(Source: Stuff.co.nz)

Most electricity generated in the world today (63.3%) is still generated by fossil fuels, and battery degradation and cold performance are both massive storage challenges electric vehicles face, not to mention the extensive amounts of infrastructure needed to lace the cities with charging stations.

Neither electric nor hydrogen vehicles are perfect. However, the lack of a balanced debate on the advantages and disadvantages of future mobility technology will likely lead to poor decisions by uninformed and misinformed, often well-intentioned organisations and governments.