Powering future mobility

Analysing the supply chains for battery electric and hydrogen fuel power packs

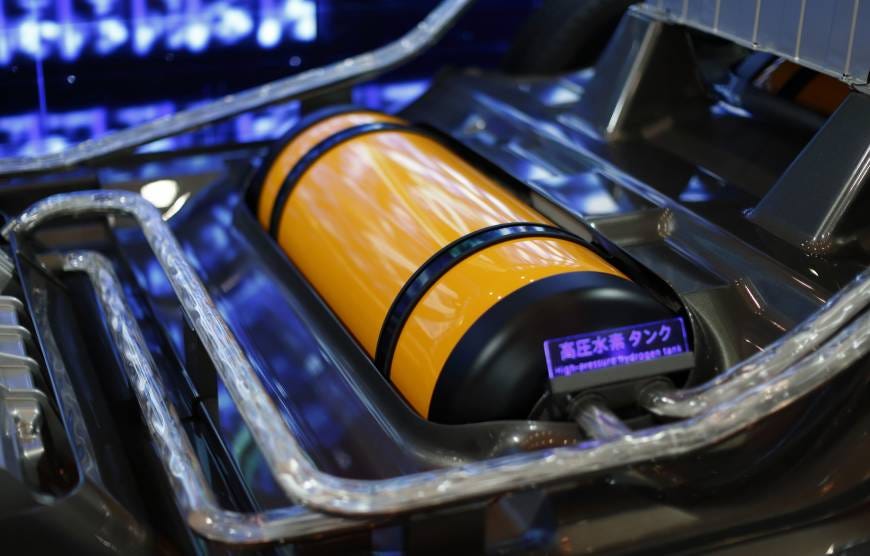

I cannot believe that I am living in an age where the fuel sources powering every aspect of our lives are about to change. It’s an exciting, interesting and really complicated journey that the world as a whole seems to have decided to embark on. Every sector is expected to play its part in this journey including road transport. Light and heavy vehicles currently emit clost to 5 Gt CO2 per year, more than shipping, aviation and rail combined. The Net Zero by 2050 IEA report points towards a key milestone of banning fossil fuel vehicle sales by 2035 on the pathway to reducing transport emissions. Many countries have already introduced bans on fossil fuel vehicle sales as early as 2025. The favoured replacement power packs at the moment are Li-Ion batteries and hydrogen fuel cells.

While everyone has been incredibly busy predicting the uptake of electric vehicles in global markets or discussing the advancesof battery and charging station technologies, few have looked at the supply chains for these power packs. In other words, we certainly have the capacity to build all the cars and trucks to sell, but do we have the raw material reserves, the mining or power pack manufacturing capacity to power all these vehicles once they’re built? So far, most analyses focus on some aspects of supply chains. For instance:

CSIRO in Australia have recently released an analysis of Lithium, Cobalt and Nickel mining capacity required to power world fleets (see report here).

The IEA published a roadmap for decarbonising light and heavy vehicle sectors stating “By 2030, electric cars account for over 60% of car sales (4.6% in 2020) and fuel cell or electric vehicles are 30% of heavy truck sales (less than 0.1% in 2020). By 2035, nearly all cars sold globally are electric, and by 2050 nearly all heavy trucks sold are fuel cell or electric.”(see report here).

The are several potential problems arising when making plans on supply chains that may be insufficiently developed for the demand. Much like the consequences of the global chip shortage affecting car manufacturers today, power pack shortages can mean inability to sell vehicles. Shortages also generally mean increased power pack prices as demand outstrips supply. These price increases would likely be reflected in the cost of new vehicles.

The Supply Chains for Vehicle Power Packs: Li-Ion Batteries and Hydrogen Fuel Cells report is our holistic exploration of what challenges and opportunities may be brought about by the transition away from fossil fuels. Clearly there are some major challenges ahead, but there are also several key opportunities which may transform the way we think and design supply chains. Read the full report here.