Tackling Europe’s Dependence on Russian Natural Gas

Russian gas seems a topic as hot as the Russo-Ukrainian conflict over the past few weeks. This edition takes a closer look at Europe’s gas consumption and at some potential solutions to this issue

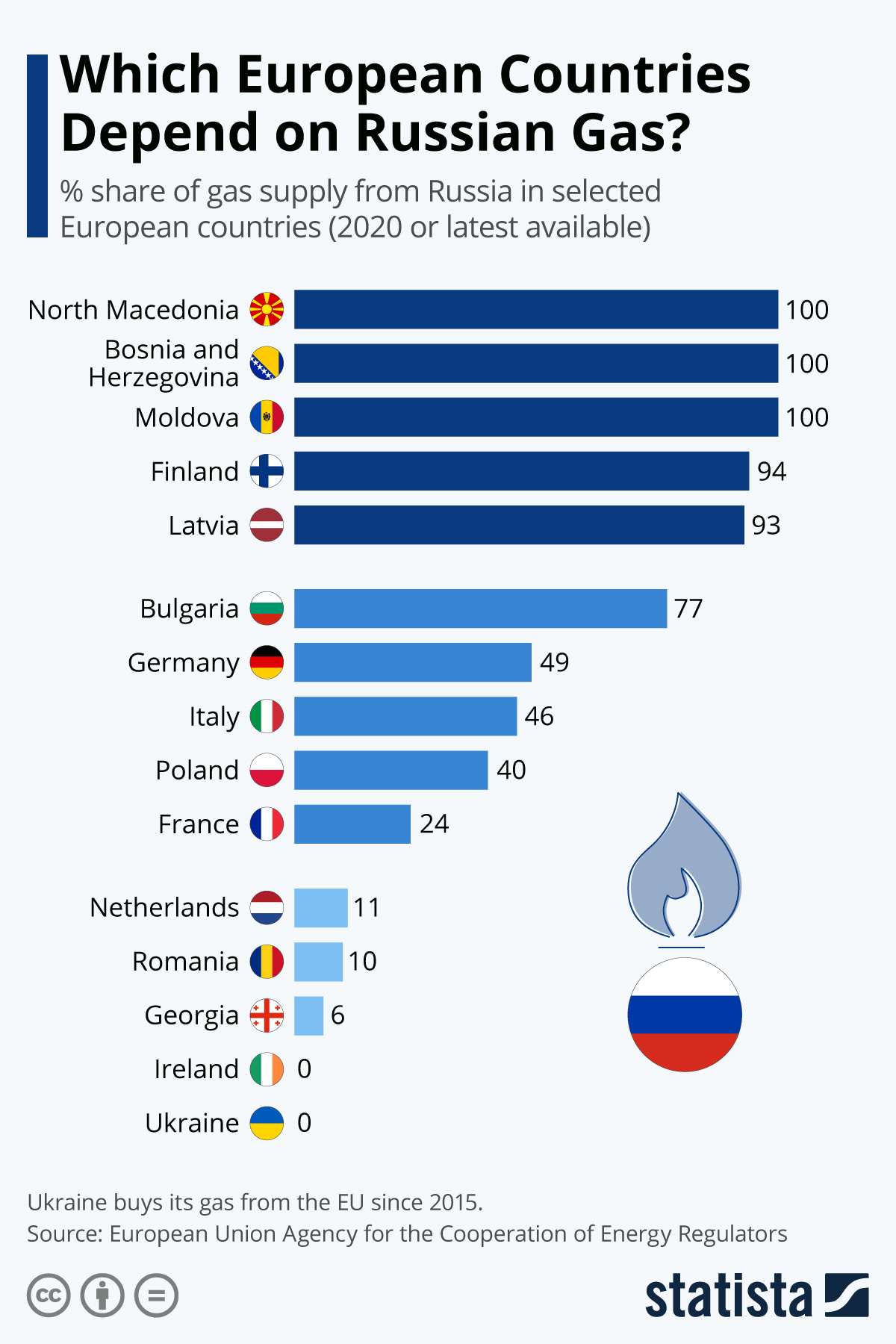

Just how big is Europe’s need for Russian gas imports? In 2020, the European Union consumed just under 380 bcm (billion cubic metres) of natural gas. This figure is down from 469.6 bcm in 2019. The decrease is massive and unfortunately just in part due to environmental policy – with the U.K.’s departure from the E.U., its gas consumption (72.5 bcm) is counted separately. Of the 380 bcm, Russian gas imports account for roughly 40% or 155 bcm. Most Russian gas is transported in pipelines (140 bcm) while the rest, 15 bcm, is exported as liquefied natural gas (LNG). Although 40% is a significant amount, some countries more dependent than others: Russian gas accounts for more than 90% of Finnish and Latvian imports, more than three quarters of Bulgarian imports and half of Germany’s.

At this point it is worth mentioning that the E.U. hasn’t stopped importing natural gas from Russia. Although many European countries have introduced sanctions, they’ve stopped short at halting gas imports. Instead, the E.U. have instead announced they will seek ways to reduce Russian gas imports from 155 to 100 bcm by 2023. I suspect that cutting the main heating source for 40% of Europe mid-February (traditionally one of the coldest months) wasn’t deemed as a sound strategic decision by European policymakers. Nonetheless, this has not stopped panic from ensuing around a potential energy crisis.

Although most news outlets have contributed to the formation of panic around the potential impact of suspending Russian imports, few have conjured up any viable alternatives. The International Energy (IEA) is one of the few to suggest potential actions in their “10-Point Plan to Reduce the European Union’s Reliance on Russian Natural Gas” including an increase in LNG imports, uptake in intermittent renewables, bioenergy and nuclear power, several end-user actions and, believe it or not, coal.

One thing that is incredibly frustrating about the E.U.’s environmental policy is the lack of consideration of time. The perceived urgency of the climate crisis means that emission reduction and energy security measures are supposed to be implemented in one or several years. Reducing 55 bcm of Russian gas imports by 2023? No problem. Building LNG infrastructure by the end of the year? Absolutely. Getting a planning approval to build an extension on your house in less than 12 months? Who are you kidding?! It took Gazprom 10 years to plan and build Nord Stream 2. Germany has yet to build its first LNG terminal even though the Brunsbüttel LNG terminal has been in the planning stage for 5 years and the terminal is estimated to be operational by 2024 the earliest. Yet, somehow, all these processes and obstacles are not an issue when it’s time to make a change for the planet.

Leaving the somewhat illusory timelines behind, I’ll go through some of the options suggested by the IEA starting from the LNG supply chain.

The LNG supply chain

Liquefied natural gas (LNG) seems like one of the most reasonable alternatives to natural gas. LNG is a particularly viable option where pipelines are impracticable – such as over vast(er) distances and oceans – thus increasing the accessible supply. Liquefaction increases natural gas’ density to levels at which sea transport makes economic sense. In fact, 1m3of LNG is roughly equivalent to 571m3 of natural gas. However, purpose-built facilities and ships are needed to establish and operate an LNG supply chain.

The key components of a simplified LNG supply chain are the liquefaction and vessel loading capacity, the ships and the vessel unloading and storage capacity. The production of natural gas at origin and consumption at destination also play a role amongst other factors.

Before going into too much detail about each stage of the supply chain, you may notice that measurement units are not the same across stages. To pre-empt the same confusion I faced:

1m3 of LNG = 571m3 of natural gas

1 ton of LNG = 0.45 m3 of LNG

Liquefaction, regasification, and storage capacity are measured in million tons of LNG per annum (MTPA).

1 MTPA is equivalent to 1.25 billion cubic metres of natural gas (bcm).

LNG vessels capacity is typically measured in m3 of LNG.

Liquefaction Capacity

The average utilisation rate for liquefaction capacity was roughly 75%. There are major differences between countries, with some (Papua New Guineea, Russia, Qatar, Oman, UAE) nearing or exceeding 100% utilisation and others (Indonesia, Cameroon, Algeria, Egypt) hovering at 50% or less. Except Algeria and Egypt, much of the export capacity is relatively far from Europe’s shores. The further the distance, the more ships are required to maintain a consistent supply and the more time it takes to establish this supply chain.

LNG Shipping

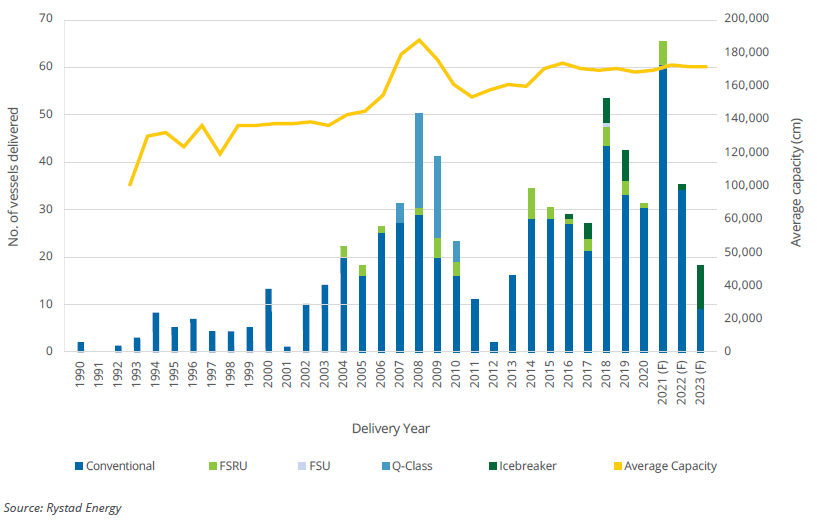

The world LNG fleet comprised of 571 vessels in 2020 with an average capacity of 170,000 m3 of LNG each. 64 more vessels were expected in 2021 and some 50-60 more are expected in 2022 and 2023. Each vessel runs on average 10.1 trips/year. Therefore, each additional ship notionally expands LNG transport capacity by just under 1bcm of natural gas/year. Clearly, some of the new ships will be servicing existing and established routes while others may be available to serve European trades. By now, the proposed 20 bcm increase in LNG imports looks achievable.

LNG Storage and Gasification Capacity

The Achille’s heel in this supply chain may well be the storage and gasification capacity on the European side. Many European facilities are already nearing capacity and recent reports have suggested that LNG storage and gasification capacity issues were already increasing before February 24th.

Notice as well that few European countries actually have LNG storage and gasification infrastructure. Germany is the most notable absence from this list. Although 4 LNG terminals have been under discussion since 2017, none have been built.

Is LNG a solution to Europe’s Russian gas dependency? It depends: on the long-term, it seems the most viable option. On the short term, it seems more like wishful thinking.

Turning Down Heaters a.k.a. Put Another Blanket On

Much like the IEA’s 10 point plan to cut oil demand which argues reducing speed limits by just 10km/h to reduce fuel consumption, the plan to reduce gas consumption IEA suggests turning down thermostats by just 1 degree to save 10 bcm/year. Is this possible? Maybe. Certainly coming into European spring and summer.

The issue I see is slightly different. When the green revolution started, I was led to believe that new technologies would lead the way froward and lead us onto a path of carbon-free plentiful energy. The reality of the green revolution seems to be settling in and it looks slightly grimmer: carbon emissions reduction through energy rationalisation. The silver bullet of renewable energy has been replaced by the cold (quite literally) reality.

If You Stare at Natural Gas Long Enough It Turns Into Coal

The cherry-on-the-cake is the ‘trade-off’ solution proposed by the IEA:

“Other avenues are available to the EU if it wishes or needs to reduce reliance on Russian gas even more quickly – but with notable trade- offs. The main near-term option would involve switching away from gas use in the power sector via an increased call on Europe’s coal -fired fleet or by using alternative fuels – primarily liquid fuels – within existing gas-fired power plants.” (p.11)

In January this year, the E.U. decided to consider gas and nuclear power as green energy. In March, Germany reactivated coal power plants to reduce reliance on Russian natural gas. In an unexpected turn of events, GAS IS GREEN BUT COAL IS GREENER. This decision does however highlight a hierarchy:

Climate is important, but politics is importanter (mistake intended).

Literally Sitting on Gas

A short term solution could potentially be available -the Groeningen Gas field in the Netherlands, the largest gas field in Europe, with estimated reserves of more than 2,700 bcm. Peak production from this field reached 88 bcm in 1976, decreased to 54 bcm in 2013 and has been declining ever since mainly due to the risk of earthquakes associated with gas production. The gas field is in the being decommissioned, a process that is being brought forward by the Dutch government.

Yes, the Groeningen Gas field is risky option. However, what are the other options? Continuing reliance on Russian gas, a thicker blanket around the waist or a billion-euro LNG infrastructure expansion programme to be completed sometime this century.