Food and Housing - Can’t Have One Without the Other

This edition explores the latest unexpected challenge in Australian food supply chains....housing?

While European counterparts are facing droughts, Dutch farmers facing forced farm buy-outs due to Nitrogen reduction regulation and urea production down 40% due to skyrocketing gas prices, Australia is heading (somewhat more slowly) to its own version of a food crisis. Aside from the potential upcoming urea shortage I wrote about in a previous post, the National Farmers Federation estimates that the agriculture sector is short of 172,000 workers. One of the main reasons… house prices! huh?!

Rents in Australia’s capital cities have increased by around 10% between July 2020 and July 2021 and another 8-10% from July 2021 to July 2022. Similar increases likely followed in regional Australia (i.e. not big cities), although statistics on this are not as easily accessible. House prices have increased by more than 25% in 2021. Several sectors including food production and agriculture are now facing labor shortages because workers cannot afford to relocate for work, especially in regional areas of Australia.

Are Workers Relocating for Work in Regional Austalia?

Some. Part of the reason for the increase in regional rents seems to be internal migration. In the 2020-21 financial year (ending in July) Greater Melbourne officially lost more than 60,000 people and Sydney lost around 5,000. A closer look at the data reveals that the losses are in fact greater. Melbourne lost 33,000 people to internal migration and 54,000 to overseas migration (so 87,000 in total) while Sydney lost around 25,000 people to internal migration and about 7,500 to overseas migration (around 32,000 in total). Both cities’ natural growth (i.e. net births) compensated for these figures, but babies don’t work in supply chains. Brisbane and Perth absorbed about 21,000 people from internal migration thus suggesting that around 90,000 people relocated in regional areas.

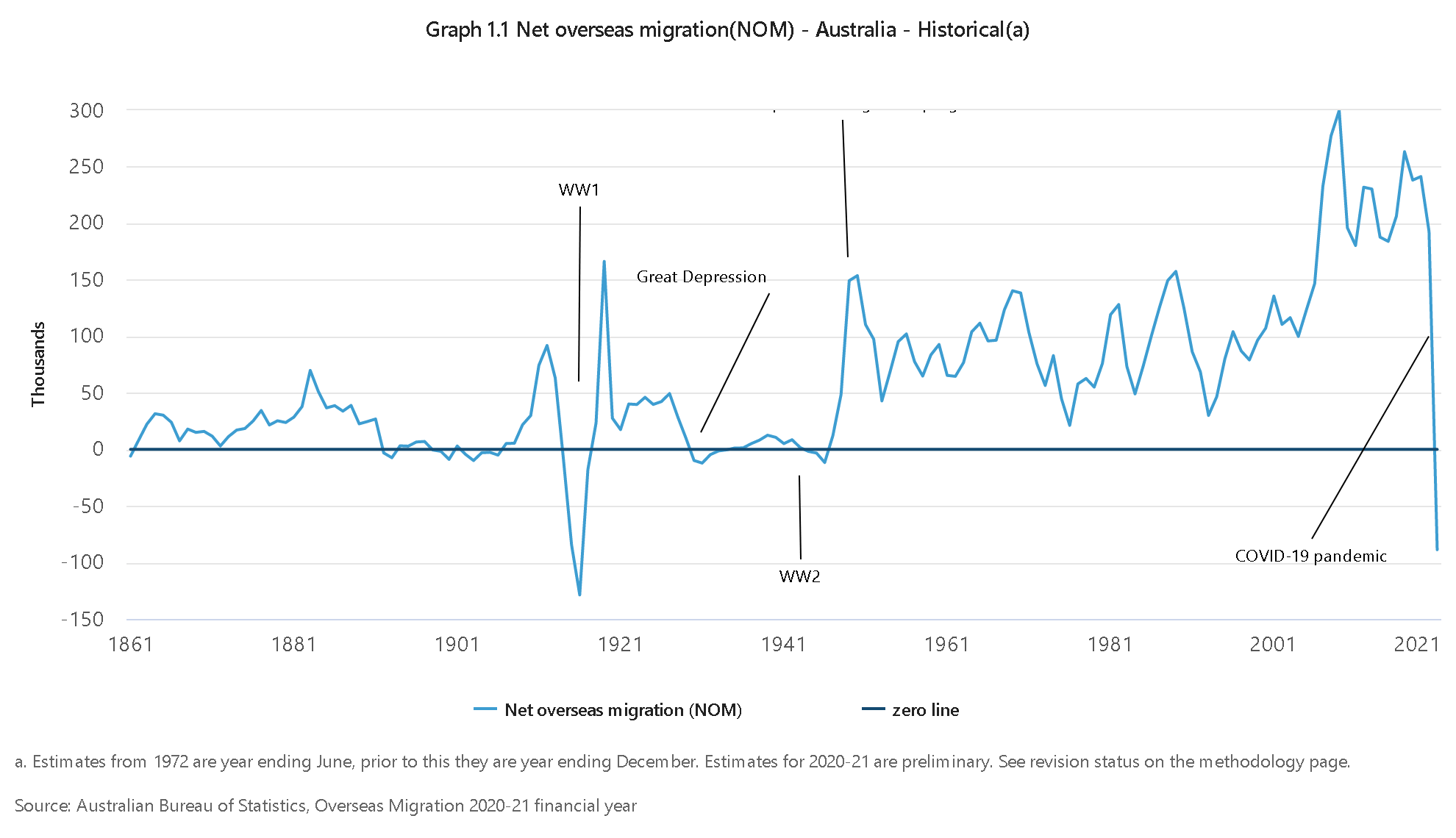

No Migration Safety Net

Overseas migration typically makes up a large proportion of Australia’s population increase, more than natural growth. Between 2016 and 2020, Australia’s population increased due to net migration (arrivals minus departures) by 200,000 people per year, while natural growth generally accounts for around 120,000 people. In 2021, net migration was minus 90,000. This means that the real estate market used to have an additional 200,000 renters or buyers each year in fact lost 90,000.

These somewhat substantial drops in demand should have a visible decreasing effect on rents and house prices but their impact is permeating through the market at an extremely slow rate.

After living in Australia for several years I can say that I have heard almost every reason imaginable for rent and house price increases, some reasons more logical than others. These range from an influx of international students and outflow of international students, increase in internal migration from capital cities (though this never seems to translate in price decreases in capital cities) and even the increase in the central bank’s interest rate which is typically used to cool off the real estate market - no joke, just have a look at the quote below from the Guardian. On very few occasions, I have experienced short lived housing price and rent decreases, one of which seems to be commencing.

“Rents have risen at the fastest rate for 14 years as Australia’s landlords seek to recoup costs in the face of rising interest rates and higher inflation.”

The Backpacker Shortage

One factor that may play a major role in food supply chains’ worker shortage, perhaps more so than house prices, is the diminished number of tourists on working holiday visas. Traditionally, around 180,000 working holiday tourists arrive in Australia, more commonly known as “backpackers”, and typically take jobs on farms or in hospitality under a variety of working conditions. Importantly, backpackers working in agriculture generally do not access the housing market because they are usually accommodated on the farms. During 2021, less than 40,000 working holiday visas were granted, a shortfall of 140,000 compared to previous years. The working holiday visitors shortfall may in fact be the largest contributor to the labor shortage experienced by food supply chains.

Two of the factors that can lead to labor shortages are a lack of qualified workers or a lack of workers willing to work for the salary offered. Australian food supply chains seem to be experiencing both. People have been leaving the country and fewer backpackers have arrived, so the worker pool has diminished. Of the workforce that has relocated to regional areas, it is unlikely that many are interested to work on similar wages and conditions as backpackers generally do.

In Other News

They Don’t Make Ship Rudders Like They Used To

Both the Suez Canal - which enables one of the busiest shipping routes in the world - and the Bosphorus Strait - which connects to the Black Sea - have been blocked for several hours earlier this month. The 250 metre Affinity V tanker and the 173 metre Lady Zehma carrying 3,000 tonnes of Ukrainian corn ran aground and blocked the Suez and Bosphorus respectively, both citing issues with navigational equipment. These two newspieces strike me as rather odd.

The Suez Canal being blocked for a few hours disrupts one or two convoys but would not typically be a newsworthy event. Why is it reported? Maybe this incident reminds people of the Ever Given grounding more than a year ago and captures a few more clicks.

The question that struck me on the Lady Zehma was why does an almost empty ship run aground? The vessel was said to be loaded with 3,000 tonnes of cargo but has a 32,000 tonne deadweight. 3,000 tonnes is close to empty. Lady Zehma’s reported draft (depth in water) was 10.3 metres which seems rather deep - Karteria, another ship loaded with Ukrainian grain with a 50,000 tonne deadweight is currently sailing at a draft of 10.1 metres. Did someone just forget to add a zero to the vessel’s cargo or what happened?

Maybe the most important question that lingers is what is happening with all these rudders?

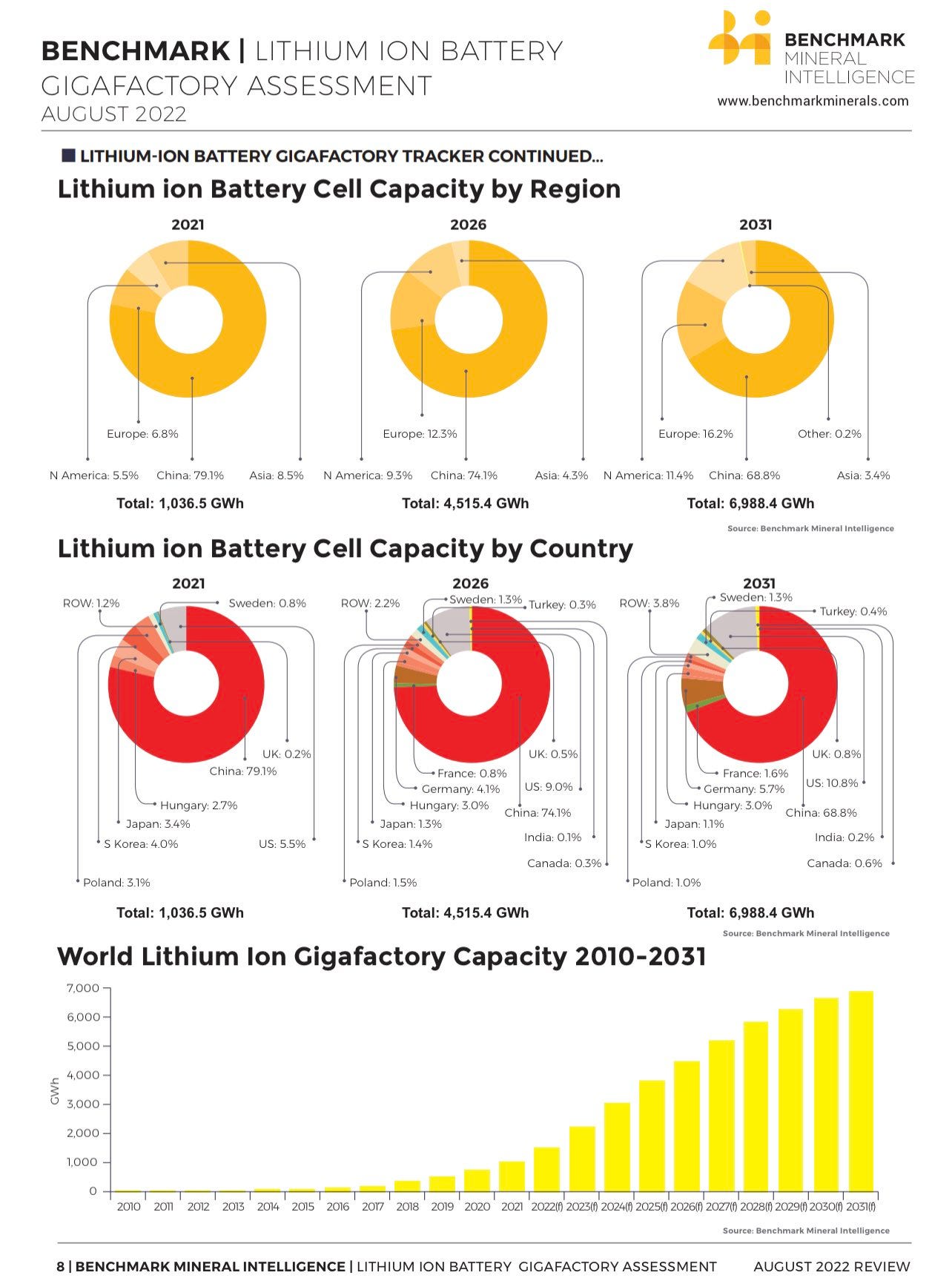

Transport Electrification at China’s Mercy

As California announced its ban on fossil fuel car sales from 2035, it may be worthwhile to reflect on Benchmark mineral’s analysis on battery manufacturing capacity. The question we drew attention to close to a year ago was whether there is enough battery manufacturing capacity to support all these bans. And the answer then was a hopeful maybe.

The next question is who owns the battery manufacturing capacity, and the answer to this question is quite clear - 80% is owned by China. You may wonder whether China will prioritise batteries for Western countries instead of its own (growing) market. One can only hope, but I wouldn’t hold my breath over it. More importantly, energy prices in Europe are inhibiting the development and growth of a battery manufacturing sector (which doesn’t happen over night) so predictions of Germany’s and France’s 7.3% combined market share by 2030 are unlikely to materialise. The Made in China label isn’t declining after all.